Orange Juice and the Price of Environmental Risk

Orange juice has long been treated as a predictable consumer staple: widely available, relatively affordable, and consistent in taste. That...

5 min read

With heatwaves sweeping Europe and North America this summer, attention has again turned to El Niño.

But its effects could extend far beyond sweltering temperatures and rising demand for air conditioning. El Niño alters atmospheric circulation and can shift rainfall and temperature patterns around the world, with potentially significant consequences for agriculture. (AP News)

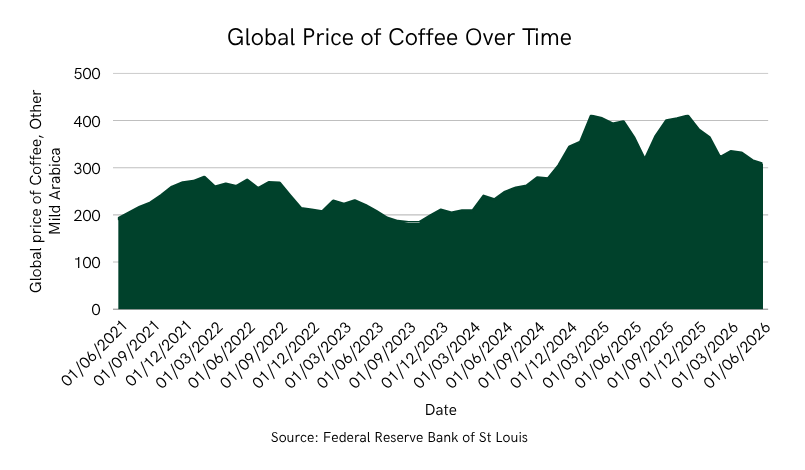

Coffee is a case in point. Prices have only recently retreated from the record highs associated with the 2023–24 El Niño and the supply disruptions that followed. With inventories still low, another period of adverse weather could quickly place the market—and coffee-dependent businesses—under renewed pressure.

In this blog post, we explore why coffee is particularly exposed to El Niño and what another event could mean for prices, supply and businesses in 2026 and beyond.

El Niño is the warm phase of the El Niño–Southern Oscillation, or ENSO, a recurring climate pattern associated with unusually warm conditions in the tropical Pacific. It can reshape weather patterns globally, contributing to drought in some regions and excessive rainfall in others. (AP News)

Coffee is particularly sensitive because production depends on favourable conditions at several points in a long crop cycle.

Rainfall helps trigger flowering. Too little rain can produce uneven flowering and reduce the number of cherries that develop. Excessive rainfall can be damaging during flowering, harvesting and drying. Higher temperatures place additional stress on coffee trees and can increase their exposure to pests and diseases. Farmers across Central America are already reporting less predictable flowering, lower yields and quality, and greater disease pressure as growing conditions become hotter and more erratic. (The Guardian)

The effects vary across the major coffee-producing regions. El Niño can bring drier conditions to parts of Southeast Asia, including Indonesia, while its wider effects on rainfall can disrupt agricultural production across several regions simultaneously. (The Guardian)

This creates the potential for correlated supply-chain disruption. A single climate event can affect several important producing regions, different coffee varieties and multiple stages of production at once.

Markets can also respond before crop losses have materialised. Expectations of drought, lower harvests or declining stocks can quickly be reflected in commodity prices.

The recent rise in coffee prices began with severe disruption in Brazil.

Drought and frost damaged the country’s 2021 crop, reducing the supply of arabica coffee from the world’s largest producer. The poor harvest contributed to a sharp fall in inventories and pushed coffee futures to their highest levels in a decade. (International Coffee Organization)

Further disruption followed during and after the 2023–24 El Niño.

Producers across Latin America faced a combination of erratic rainfall, heat, disease and labour shortages. In Central America, farmers have reported disrupted flowering cycles, declining yields and quality, and rising production costs. (The Guardian)

Vietnam, the world’s largest robusta producer and second-largest coffee exporter, also plays a central role in global supply. Because Brazil and Vietnam together account for a substantial share of world coffee exports, adverse conditions in either country can have an outsized effect on prices and availability.

Low inventories magnified these pressures. When available stocks are limited, buyers have less protection against weak harvests, and forecasts of further disruption can produce larger price movements.

The result was a sharp rise in both arabica and robusta prices. Retail prices subsequently increased as roasters and manufacturers passed at least part of the higher cost of beans on to consumers. Weather-related supply constraints, strong demand and, in some markets, tariffs continued to support elevated prices into 2025. (MarketWatch)

Although coffee prices have since eased, the market remains exposed. Producers are still contending with higher temperatures, irregular rainfall, labour constraints and depleted financial buffers. (The Guardian)

For coffee-dependent companies, higher commodity prices increased procurement costs, absorbed working capital and placed pressure on margins.

The broad transmission mechanism was relatively straightforward:

Higher coffee prices → higher operating costs → consumer price increases and efficiency measures → pressure on margins and sales volumes.

JDE Peet’s provides one of the clearest examples because of its concentrated exposure to coffee and tea. In 2025, the company reported approximately €1.6 billion of cost inflation, driven substantially by higher green-coffee prices. It increased prices by 19.5%, which helped organic sales rise by 15.3%. However, volume and mix declined by 4.3%, while adjusted EBIT increased by only 1.2%. (JDE Peet’s 2025 full-year results)

Nestlé experienced a similar effect. Its gross margin fell by 110 basis points to 45.6% in 2025, with the company identifying higher coffee and cocoa costs, alongside tariffs and foreign-exchange movements, as contributors. Pricing and cost savings partly offset the increase in commodity costs, but were not sufficient to prevent the decline in margin. (Nestlé Annual Report 2025)

The effect was also visible at Lavazza. The company’s revenue rose to €3.9 billion in 2025, but its EBITDA margin declined from 9.3% to 8.8%. Lavazza attributed the pressure partly to record green-coffee prices and responded through tighter management of inventories and working capital, supply-chain efficiencies and changes to its product portfolio. (Lavazza Group 2025 financial results)

These examples illustrate the commercial trade-off facing coffee companies. Passing higher input costs on to customers can protect revenue and earnings, but may also weaken demand or encourage consumers to move to cheaper products, brands or channels.

The financial impact is also broader than the income statement. More expensive beans increase the amount of cash tied up in inventory. Companies may need to fund purchases earlier, carry larger stocks or pay more to secure particular origins and grades. Shortages can also affect blends, product quality and logistics costs.

The scale of the impact will vary considerably. Larger businesses may benefit from greater purchasing power, more diversified sourcing and stronger access to finance. Smaller roasters and retailers may face more immediate pressure because they have less capacity to absorb higher costs, hold additional inventory or negotiate favourable supply terms.

The developing 2026 El Niño is forecast to be substantially stronger than the 2023–24 event.

NOAA’s Climate Prediction Center estimates an 81% probability that it will reach the “very strong” category during the final months of 2026, potentially placing it among the strongest El Niño events recorded since 1950. It is also expected to persist into early 2027. (Climate Prediction Center)

That does not determine the precise impact on coffee. Outcomes will still depend on where drought, excessive rainfall and extreme temperatures occur during the crop cycle.

However, if a stronger El Niño disrupts several major arabica and robusta regions at the same time, the effect on coffee production, availability and prices could exceed what was seen during the previous cycle. That is a risk scenario rather than a firm forecast, but the combination of a potentially historic El Niño and an already stressed coffee supply chain raises the prospect of a more severe shock. In fact, forecasts suggest that El Niño could cut Brazil's harvest by up to a fifth due to excessive heat and irregular rainfall. (Reuters)

For businesses, this could mean another period of commodity inflation, higher working-capital requirements, further consumer price increases and renewed pressure on margins and sales volumes.

Companies cannot prevent El Niño, but they can reduce the extent to which it becomes a financial shock.

The first step is to understand exposure at a more detailed level. Businesses need to know not only how much coffee they buy, but which origins, varieties, qualities and suppliers they depend on. A supply chain that appears diversified at country level may still rely heavily on one region or type of coffee.

Inventory can provide a buffer, although holding more stock increases storage and working-capital costs. Companies can also review their ability to substitute between origins or adjust blends without materially affecting product quality.

Businesses should stress-test the implications of a more severe event. This includes assessing the effects of higher prices, lower supply, longer lead times and weaker consumer demand together, rather than treating commodity inflation as an isolated risk.

The longer-term response sits further upstream. Supporting producers with improved agronomy, disease management, shade, soil health and more resilient coffee varieties can reduce the likelihood that adverse weather develops into a severe crop failure. Stronger supplier relationships and more geographically diverse sourcing can also improve access to scarce coffee when markets tighten. Farmers in Brazil are already reporting that their crops are more resilient compared with previous El Niño episodes thanks to technological advances producing a more climate-resistant crop. (Reuters)

The previous El Niño cycle has already shown how quickly weather disruption can move through commodity markets and into consumer coffee prices.

The more important question is whether businesses could withstand a larger shock without unacceptable consequences for margins, cash flow, product availability or consumer demand.

With the 2026 El Niño forecast to become one of the strongest on record, that resilience may soon be tested again.

Orange juice has long been treated as a predictable consumer staple: widely available, relatively affordable, and consistent in taste. That...

For years, nature-related risk sat in a grey zone - acknowledged, discussed, but rarely acted on. In 2025, that changed. Rules became clearer....

Nature is no longer a peripheral sustainability issue. From water scarcity and land-use change to biodiversity loss and tightening regulation,...